Big brands are the knock-out winners in a recent eBrand ranking (1) of performance in UK online retailers, despite the popular view that big brands are losing out to smaller, more digitally savvy insurgent brands in this channel.

Online retail (e.g. Tesco online, Amazon) is a critical channel as although it is still small, it is growing quickly. It accounted for 90% of US consumer goods growth in 2017 (2).

To note, this post focuses on eCommerce retailers, not ‘Direct to consumer’ eCommerce, where a handful of small insurgents have made big headlines, although not always big profits (e.g. Dollar Shave Club was sold to Unilever for $1billion despite being loss making).

The hype …

Small, ‘insurgent’ brands are much more digitally savvy than big brands, according to the headlines of online news sites and consultancy research papers. In particular, so the story goes, small brands perform stronger versus big brands in ecommerce than they do in physical stores. “Today, (small brands) find willing customers in fast-growing new retail formats, especially premium, convenience, and online … (where) shelf space is unlimited: small brands often have the same visibility as large ones,” claims BCG, for example (3).

… the reality

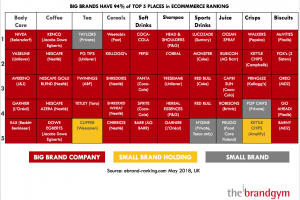

As our summary below illustrates, big brand companies (red) have 94 out the top 100 positions in the eBrand Ranking, which gives a top 5 brand list across 10 ecommerce categories. Small insurgents (grey) have a mere 4 winners (Pop Chips, Taylor’s of Harrogate tea plus 2 slightly weird Polish food brands, including a 25p Red Bull rip-off called N’Gine sold in Tesco). A further 2 brands are owned by ‘small brand holding companies’ (orange), who have acquired a portfolio of smaller insurgents.

Further evidence of big brand strength in ecommerce came from an interview with Roisin Donnelly, former brand director for Northern Europe at P&G, done as part of our research project on ‘Big Brands Under Attack’. She explained how P&G brands aim for a bigger share in ecommerce than they have in physical stores. This is shown by Tide detergent having a much bigger share in the online space (48%) than in the market overall (38%).

So, why do big brands, not small ones, seem to be winning with eCommerce retailers?

1.Memory structure matters even more in ecommerce

Big brands, if managed well, have strong ‘memory structure’: hard-wired’ associations, related to trusted functional performance, emotional connection and brand properties (logos, colours, symbols), built up over many years or even decades. This memory structure gives big brands much stronger top-of-mind awareness than smaller brands. When you think of a category, a big brand is likely to come up first. Only on reflection do smaller brands start to pop into your head, and often only when prompted (“Have you heard of brand x of dogfood?”)

This memory structure advantage is especially important in eCommerce, where a lot of grocery shopping is done in ‘system 1’ mode. You look at an online shopping cart on your PC or smartphone, and think of a category, say toilet paper. ‘Bam!’, a brand comes to mind on ‘auto-pilot’. And the chances are, this will be a big brand, owing to its superior memory structure.

You have less visual distraction than a physical store to tempt you into ‘system 2’ mode, where you start browsing and considering alternatives. Yes, there are promotions, but they are less visible. Indeed, only 10% of online shopping is done ‘on deal’, compared to a massive 70% in physical stores, according to experience Roisin shared with me from her P&G days.

2.The power of the shopping list

The memory structure advantage of big brands is amplified in ecommerce retailers by the use of shopping lists. These lists allow you to start your shop using terms like ‘Your favourites’, ‘Last order’ or ‘My usuals’, as you can see in the example from Tesco online below.

So, once a big brand gets onto one of your lists, it is hard to budge. Shopping lists are classic system 1 time-savers, making your life easier by reducing the effort you have to put into making a decision.

The use of online shopping lists may also explain the lower levels of promotional shopping discussed earlier.

3.Big brand alliances

Big brand have much more human and financial firepower to partner with online retailers than small brands, and this should give them an important edge.

Using P&G again as an example, the company bought 1% of UK online grocery retailer Ocado to learn about ecommerce, and has been an early adopter of Amazon initiatives such as Amazon Dash re-ordering buttons and Subscribe and Save.

Check out the image below, used by Amazon to promote Amazon Dash. Spot any small insurgent brands? Nope. All the brands are big brands, as these are the ones that most people want to re-order most of the time, and because big brand companies are the ones Amazon will want to partner with to promote the service.

Conclusions

In conclusion, this survey shows that big brands should be aiming to have an even bigger edge vs small insurgent brands in the eCommerce channel versus physical bricks & mortar retail. Key to success are actions including:

1. Create and amplify memory structure through ‘fresh consistency’ over time and over the mix, so your brand is top-of-mind

2. Invest in partnerships and alliances with online retailers to build knowledge of and shape practice in the ecommerce space

3. Renovate your brand mix and push to regain space in physical retailers that has been given to small brands. Despite sometimes having lower rates of sale, small brands have won more than ‘fair share’ of space with contemporary, natural and healthy brand positionings that appeal to retailers.

4. Investigate direct-to-consumer opportunities, but in most cases this will be more profitable by partnering with online retailers for fulfilment (e.g. Gillette using Amazon’s Subscribe and Save service to compete with Dollar Shave Club and Harry’s)

Sources:

1. https://www.ebrand-ranking.com/categories

Run by mySupermarket Business Solutions and checked/endorsed by Kantar Consulting. Uses 10 KPIs combining webcrawling of UK grocery e-retailers’ data and an online shopper panel comprising tens-of-thousands monthly online transactions.

3. http://www.nielsen.com/us/en/insights/news/2017/as-us-retail-shifts-continue-e-commerce-thrives.html