Investment bank Goldman Sachs announced this week that it was retreating from its attempt to fully stretch into consumer banking, six years after launching the Marcus brand. “After product delays, executive turnover, branding confusion and deepening financial losses, the firm was pivoting away from its previous strategy of building a full-scale digital bank,” reported CNBC (1). This is a dramatic change of direction. As recently as April 2022 the firm said it intended on becoming the leading consumer digital bank in the world (2).

In this post, we look at the lessons we can learn about brand stretching and new brand creation from the Marcus mis-steps.

1. The need for a new brand is a warning sign

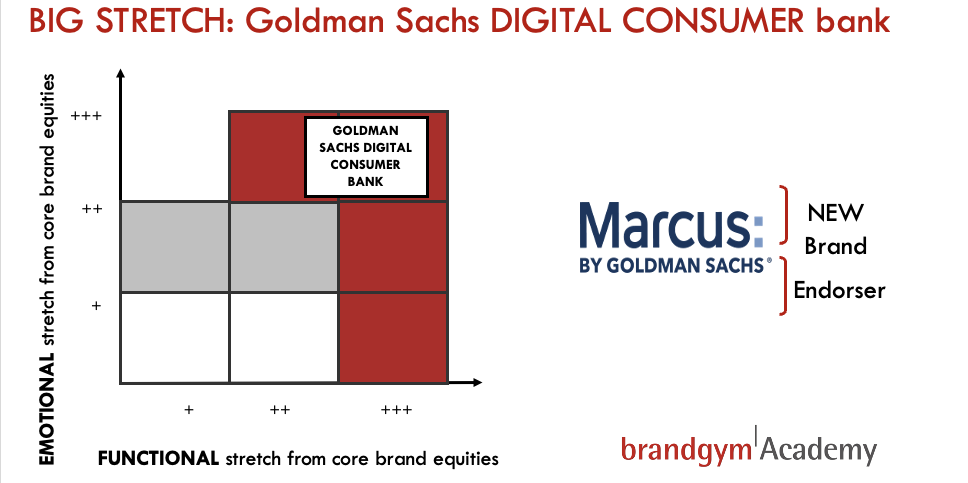

Goldman Sachs is a business-to-business (B2B) brand famous for investment banking. For 147 years, the bank stuck to its core businesses of investment banking, securities and investment management. Then, in 2016 the company made a bold move by stretching into consumer banking. The fact that Goldman Sachs needed to create a new brand for this launch should have been a warning sign. It showed that the brand stretch from the core was big, on two dimensions.

From a functional standpoint, the competences to deliver consumer banking are different from investment banking. Consumer banking requires excellence in business-to-consumer marketing, including call centres, customer experience design and digital marketing.

But the biggest stretch was from an emotional standpoint. Marcus was “an attempt by the world’s most powerful investment bank to be seen as a cuddly, quirky consumer’s friend,” reported The Times back in 2018 (3). “The Wall Street giant earned the unflattering moniker of “a giant vampire squid” for its predator-like tendencies. By contrast, Marcus has been likened to a “loveable teddy bear” by its American boss, Harit Talwar.”

Action point: if a new product or service launch is such a big stretch from your core that a new brand is needed, challenge yourself to ask if this is a stretch too far

2. Look at ability to win, not just size of prize

SIZE of the PRIZE is the first key question to ask when assessing the long term viability of a brand stretch attempt. And on this dimension, Marcus has made quite an impact in the marketplace. It has acquired 15 million customers and more than $100 billion in deposits (4). Net revenue in the last quarter was $744million, almost double the same quarter in 2021.

However, the second question to ask is ABILITY to WIN. This questions looks at whether you have the core competences to compete in the new market and the cost of launching and sustaining the new business. And it is on this second dimension where many brand stretch attempts, including Marcus, run into problems. Marcus had to offer a high interest rate of 1.5% to get customers to switch, in a market where consumer inertia is a real challenge. Awareness had to be built and maintained for the new brand. New systems and infrastructure needed to be created, maintained and continually upgraded. As a result, Marcus is on track to lose $1.2 billion in 2022. The continued heavy losses are in stark contrast to the 2020 Investor Day presentation. At the time, the firm forecast that consumer and transaction banking would break even in 2022 and generate positive returns in subsequent years (5).

It seems that CEO David Solomon belatedly recognises that Goldman Sachs lacked the ability to win in stand-alone consumer banking. “The concept of really being broad with a consumer footprint is not really playing to our strengths,” he is reported as saying to CNBC (6).

Action point: when assessing a potential brand stretch, look not only at the size of the prize but also your ability to win.

3. Stretch to grow the core business

Brand image benefits are often used as a rationale for brand stretching, as was the case with Marcus. “Done well, this is reputationally enhancing,” said Goldman’s UK treasurer David Bicarregui at the time of the UK brand launch. However, these so called ‘image halo’ effects often turn out to be a mirage.

Rather than looking for image benefits, I recommend focusing on brand stretch initiatives that have core business benefits. We looked at how Netflix’s stretch into content creation helped enhance and grow the core streaming offer in an earlier post here.

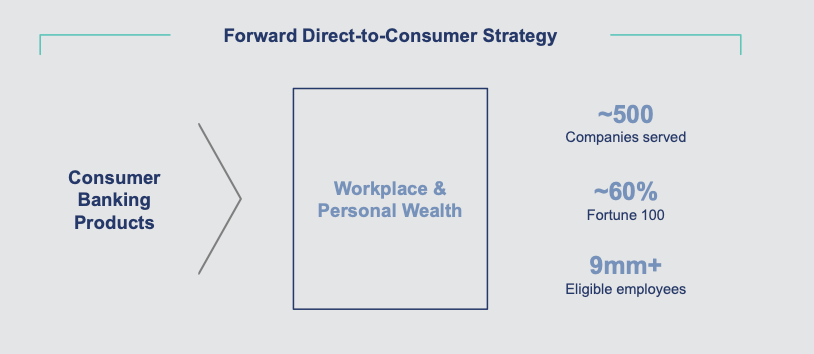

Encouragingly, Goldmans seem to be now adopting this approach of brand stretching that builds on AND benefits the core business. In a major reorganisation, consumer banking will become part of the wealth management unit. “Rather than seeking to acquire customers on a mass scale for the business, Goldman will aim to market fintech products through the bank’s workplace and wealth management channels”, according to CNBC (1). The wealth management business was “a better place for us to be focused than to be out massively looking for consumers,” Solomon is reported as saying.

In this way, the firm is leveraging its strengths in its core workplace and wealth management channels to grow consumer banking (see below). In this way, Goldman can access millions of high income consumers it already interacts with, rather than spending heavily on marketing to steal consumers from competitor banks. At the same time, a personal banking offer can help enhance the core service offering.

Action point: don’t just look at potential brand image benefits of any brand stretch idea. Look also at the potential of the brand stretch to directly benefit the core business offering

In conclusion, Goldman Sachs’ retreat from consumer banking shows the challenges of stretching your brand the need to assess your ability to win, not just the size of the prize, when considering such a move.

To explore BRAND STRETCH in depth we offer a short, on-demand course on our brandgym Academy platform here.The course is only £95+VAT and is fully refunded if you go on to take the full brandgym Mastering Brand Growth program where we explore a comprehensive and practical 8-step program for creating brand strategy to inspire business growth.

For more on the challenges of brand stretching, see this earlier post.

Sources