J Sainsbury recently announced it was giving up on its ambitious attempt to stretch from supermarkets into banking, with plans to wind down Sainsbury’s Bank. This is a big call to make, given than Sainsbury’s has managed to acquire 1.9million customers and is making a profit from this operation.

In this post, we look at the rationale for the bold move and the learning on brand stretching.

Click below to listen to the brandgym podcast version of this article:

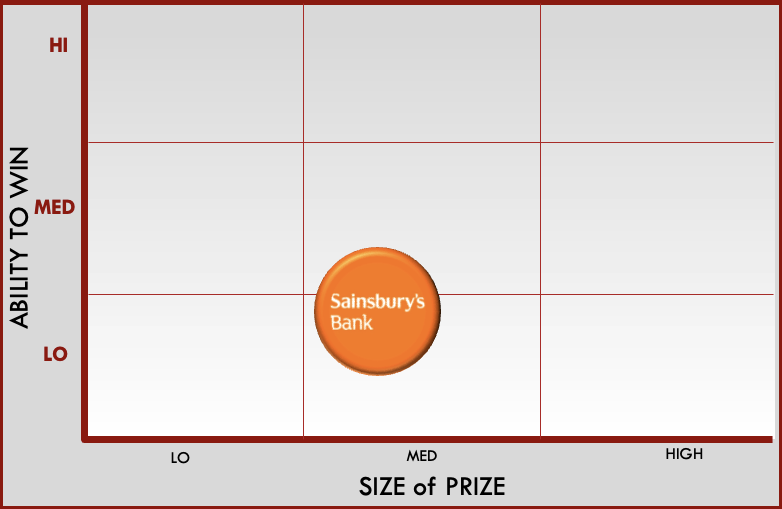

1. Look at ability to win, not just size of prize

SIZE of the PRIZE is the first key question to ask when assessing the long term viability of a brand stretch attempt. And on this dimension, Sainsbury’s made quite an impact in the marketplace. It managed to acquire 1.9 million customers since stretching into banking in the late 1990s. It had almost half a billion pounds of mortgage deposits (1) and made £60million in profits as its peak (2).

However, the second question to ask is ABILITY to WIN. This questions looks at whether you have the core competences and scale to compete in the new market. It also looks at the cost of launching and sustaining the business. And it is on this second dimension where many brand stretch attempts run into problems.

Banking today requires heavy capital commitment and onerous compliance processes. Big banking brands can spread these costs over a sizeable business, in contrast to a niche player like Sainsbury’s. The heavy cost burden in relation to the size of Sainsbury’s banking business is reflected in declining operating profits (£13million in half year to November 23, down -£6million versus year ago). This might lead us to now rate the ability to win for Sainsbury’s Bank as LOW (see below).

In contrast, the Co-operative bank that bought Sainsbury’s mortgage book has a total of £19.6billion in mortgage deposits, almost 40 times the scale of Sainsbury’s (3).

Action point: when assessing a potential brand stretch, look not only at the size of the prize but also your ability to win.

2. Focus on the core

Under previous CEO Justin King, Sainsbury’s was committed to brand stretching. The bank was originally a 50-50 joint venture with Bank of Scotland. However, King “doubled down on the venture in 2014, paying £248 million to buy out Bank of Scotland’s share”, as The Times reports (2). In contrast, the strategy led by current CEO Simon Roberts is quite different.

Back in 2020, Roberts launched an initiative called ‘Food First’. This strategy was designed to “Put food back at the heart of the supermarket’s offer, reset its competitive position and create a strong financial platform from which to grow.” (4) This clear strategy means that all investment can be focused on the core. Furthermore, the top talent in the business is also focused on the core. “We have been clear since we launched our Food First strategy that we would concentrate our efforts on our core retail businesses,” announced Roberts (2). “And today’s announcement reflects that strategic focus.”

Action point: when considering a brand stretch idea, check if this idea will directly benefit the core business. If not, challenge the team to consider if time, talent and money would be better focused on growing the core.

3. Consider other ways to innovate

Sainsbury’s has millions of customers and a strong brand image for quality and service. Offering financial services to these customers has the potential to enhance the overall brand proposition and create incremental revenue. The issue, as seen above, is the ability win and in particular to get scale. This is reflected in Sainsbury’s decision to not withdraw from banking altogether. Rather, Sainsbury’s will offer these services through partners, allowing them to focus on the core food business. “Financial services products that we continue to offer in the future will be provided by dedicated financial services providers through a distributed model,” the company announced (2). “We already do this successfully with our insurance products.”

Action point: when considering a brand stretch idea, if ability to win is low but size of prize is strong, explore if a third party could help deliver the new product or service

In conclusion, Sainsbury’s retreat from consumer banking shows the challenges of brand stretching and the need to assess your ability to win, not just the size of the prize, when considering such a move. Tesco is also said to be looking at selling its banking operation, with Barclays a potential buyer, according to The Times (2). So, watch this space to see if they follow the same strategy to ret-focus on the core.

To explore BRAND STRETCH in depth we offer a short, on-demand course on our brandgym Academy platform here. The course is fully refunded if you go on to take the full brandgym Mastering Brand Growth program where we explore a comprehensive and practical 8-step program for creating brand-led growth.

For more on the challenges of brand stretching, see this earlier post.